Ultimately - banking technology as well as large information are high up on the program for monetary services C-suites. Banking leaders identify that the capacity to essence as well as use information held within their service operations - and to automate document procedures in their value chain, offer remarkable competitive advantage. Meanwhile, as open banking becomes a fact of life for both consumers and also financial institutions, it introduces new avenues for producing income streams.

However, in numerous organisations, there are barriers blocking those chances. Occasionally it's financial restraints; other times, it's simply a lack of assistance and/or understanding throughout the business.

Right here are 5 pressing factors to re-prioritise intelligent document handling (IDP) in your electronic change program, and knock down those barriers one by one.

1. Huge data in financial is a major, unmissable possibility

As challenger banks continue to interrupt the economic solutions landscape, conventional financial institutions have one terrific advantage-- the massive amounts of information they hold relating to their client bases and also segments. Funding applications alone produce mountains of information to please back-end procedures. However this information isn't always in a form that can be accessed; neither is it confirmed for its integrity.

Being able to automatically interpret customer records for smart insights opens useful information for financial institutions, which can then be fed right into other areas of the business, or into applications. From there, banks can create products to satisfy the demands of retail, SME and business consumers as well as dissolve their discomfort points; they can boost the client experience, and allow financial health and wellbeing conversations between customers and the sector.

Data powers personalisation, opening communication with consumers regarding products at the right time, in a manner that makes good sense to individuals. Consumer data comes to be a source to form method.

IDP uses a set of technologies - from expert system (AI) and artificial intelligence (ML) to optical character recognition ( OPTICAL CHARACTER RECOGNITION) and also natural language processing (NLP). These enable financial institutions to record, categorize, as well as essence data saved in papers, turning disorganized and semi-structured information into a structured style.

Intelligent automation modern technology can after that be put on the removed data for improved validation as well as to automatically enter it into existing applications. Advanced analytics permit reporting and understandings in real time from digital banking solutions numerous resources, so organisations can consume, analyse as well as execute on the insights, feeding right into the financial institution's worth proposal.

2. The COVID result: brand-new assumptions from end consumers

With social distancing limitations, lockdowns and also a mass work-from-home motion in lots of markets, we have actually seen a transformation in consumer involvement.

It began with a mass trip to digital networks throughout both retail and also industrial banking, accompanied by skyrocketing download prices for applications, especially in the early months of the pandemic.

" The banks are currently reprioritising their digital transformation programs," says Sandstone Technology CEO Michael Phillipou.

" 18 months earlier, a bank might have had a roadmap of 3 years of programs they were mosting likely to be addressing. Now they realise they require to accelerate that investment, reprioritise some of those programs, and also generate new concerns to ensure they've obtained market-leading digital value recommendations."

" This speed as well as dexterity is something we have actually never ever seen prior to," Phillipou says.

Overnight, electronic options have actually been established to fulfill consumers' requirement for safety as well as benefit, as well as cashless settlements as well as global settlements have ended up being a must.

" We likewise instantly saw a demand for pleasure principle," claims Phillipou. "Getting answers promptly and also being able to communicate with your bank, either by self solution or by a banker on the other side, are now anticipated as a matter of course."

Keep in mind that in an setting of boosting cybersecurity violations, brand-new financial modern technology needs to be stabilized with conformity, info safety and also threat administration. "If payment systems were to go down, that would certainly have a devastating result economically and also ruin rely on organizations," Phillipou says.

3. Digital loaning services will certainly constantly have heavy conformity obligations

Banks have a traditional profile as well as appropriately so. They have significant as well as ever-changing regulatory commitments to abide by, and layers of stakeholder authorizations to secure prior to onboarding any type of brand-new capabilities.

" Therefore, established financial institutions normally aren't modern technology leaders," Philippou says.

However there is a massive opportunity for financial institutions to enhance their capability to fulfill regulatory compliance swiftly and quickly-- through automated IDP products like Sandstone's queen.

DiVA gives consumers verified and auditable regulatory compliance via an integrated guidelines engine with no code setup required.

And also since queen is Software Program as a Solution, it's rapid to implement. A financial institution might conceivably set up IDP throughout their business in a matter of weeks.

" This is what financial technology will certainly appear like across the board in the future," Phillipou says. "Cloud indigenous, cloud based, API initially, containerised, with microservices-- all of these with each other enable rapid implementation and also rapid realisation of advantages. Being intake based, the product can be switched on and also off swiftly."

4. The drive for efficiency gains across the board

According to Phillipou, from the bank's point of view, every board is being asked to do three points. The very first is to increase their return on resources, which suggests expanding their properties, their lending publications as well as responsibility books.

The 2nd: they require to currently do even more with much less, by decreasing their cost-to-income proportion. And also ultimately, number 3 is to adhere to all guidelines and also stay clear of penalties.

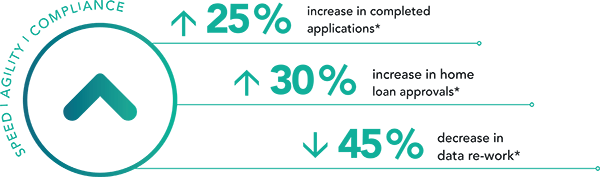

" When it come to the second point, this is definitely an effectiveness play," Phillipou states. "The best electronic financing option will result in decreased time to process car loans, and that's the main use case our clients are using our capability for. Intelligent paper handling is a vital part of that."

With smart automation, banks can begin to provide financings bent on customers at a much better rate than they might have or else. Personal details can be redacted, files can be revolved as well as analyzed as well as indexed. As well as with more precision in the method they refine information, as well as little or no re-keying of info, the error rate with customers is far reduced.

As the process comes to be extra effective for organisations, they can redeploy those back-office resources right into other locations where they can gain a higher impact. It has to do with expense savings for customers as well as a far better consumer experience with less pain points.

Ultimately banks are working towards the concept of right via processing (STP): absolutely digital processing of monetary purchases from the factor of initial 'deal' to final negotiation, entailing no hands-on treatment. The goal is to attain better speed, accuracy, integrity and also scalability.

5. The open banking future counts on excellent, big data in financial

The staged intro of open banking as well as the opening of APIs to third parties has actually been an additional inspiration for change, assisting change industry focus onto the value of information integrity and access.

Financial institutions require to be able to seize the opportunities this offers. That includes opening 'marketplaces' to assist construct out their own product collection and also consider new profits streams for business. These might include anything from re-selling to economic insights for retail as well as organization financial.

As Philippou claims, "From our side, as a modern technology companion, we're seeing even more ask for solutions to meet these requirements today."

There is no question that financial institutions must be information driven if they intend to offer much better financial product or services to fulfill consumers' demands as well as assumptions; as well as if they want to make the most of opportunities as they occur.

At the same time, they require to drive efficiency and also performances throughout business, while reducing functional threat. The moment has pertained to adjust, and do it promptly.